Finland has moved beyond AI curiosity. Now it must prove it can scale

Finnish companies are adopting AI at a faster pace than ever. But adoption and impact are not the same thing. Drawing on four primary data sources — including FAIR’s own consultancy findings — this article examines why the gap between AI activity and measurable business value persists, and what it will actually take to close it.

Text by Dr Umair Ali Khan & Martti Asikainen, 27.5.2026 | Photos created with AI

AI adoption in Finnish enterprises is progressing steadily in 2026. Our AI consultancy work in the Finnish AI Region (FAIR) project shows an increasing number of companies integrating AI into their core business, products, and services. The country appears digitally capable, increasingly active in AI adoption, and well-positioned in several areas of applied AI. However, current studies raise questions about the overall impact of AI on business growth and productivity, suggesting that an increasing trend in AI adoption does not necessarily translate into greater business impact.

But what is the reason for the gap between AI adoption and business impact in Finland? Here is a pattern we encounter regularly at our consultancy work. A company has introduced an AI writing tool, perhaps a coding assistant, and has run a pilot in one department. Leadership is broadly supportive. Someone has attended a conference. And yet, when you ask what has changed in how the company creates value or competes, the answer is quieter than the enthusiasm suggests.

This is not a Finnish peculiarity, but Finland offers a particularly clear illustration. According to AI in Finnish Business 2026 (Demos Helsinki 2026), the share of advanced AI companies has more than quadrupled in two years. That sounds like progress. The same report also notes that more than half of organisations remain in the assessment and preparation phase, and that AI use across many companies remains fragmented, individualised, and supported by small experimental investments.

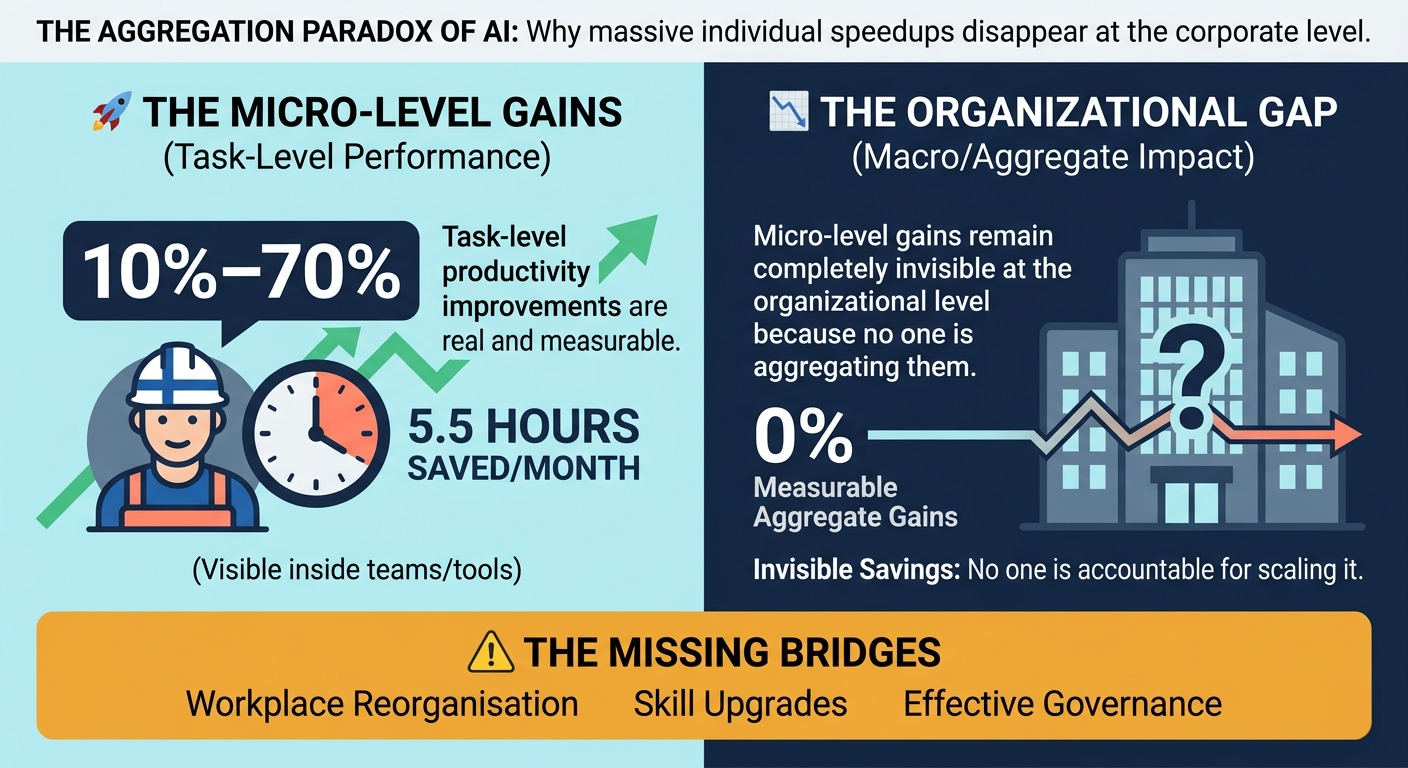

Both things are simultaneously true, and the tension between them is the story. Recent ILO analysis gives this tension a name: the aggregation paradox of AI, where substantial task-level productivity improvements — typically in the range of 10–70 per cent — fail to translate into measurable organisational or macroeconomic gains. Translating micro-level gains into aggregate productivity growth depends on broad diffusion, complementary investment in workplace reorganisation and skills, and effective governance (Chan & Shedania 2026).

Finnish AI Dilemma

Finland’s AI situation is both promising and concerning. Finland may be good at understanding, experimenting with, and regulating AI, but slower at industrialising it. While more companies are beginning to use AI at the core of their business, products, and services, AI use across many companies remains fragmented, individualised, and supported by small experimental investments (Demos Helsinki 2026).

This is the core of the Finnish AI debate in 2026. The issue is not whether Finnish companies have noticed AI. They have. The issue is whether they can connect AI to strategy, value creation, investment, and scaling. Part of what makes this difficult is that the absence of a strategy is not a neutral position.

The vacuum fills immediately with whatever individual employees find useful and accessible — and by the time a formal strategy arrives, the workflows are already established and the habits already formed (Asikainen 2026a). We have also emphasised strategy and value creation in our earlier articles (Khan 2024; Khan & Asikainen 2026).

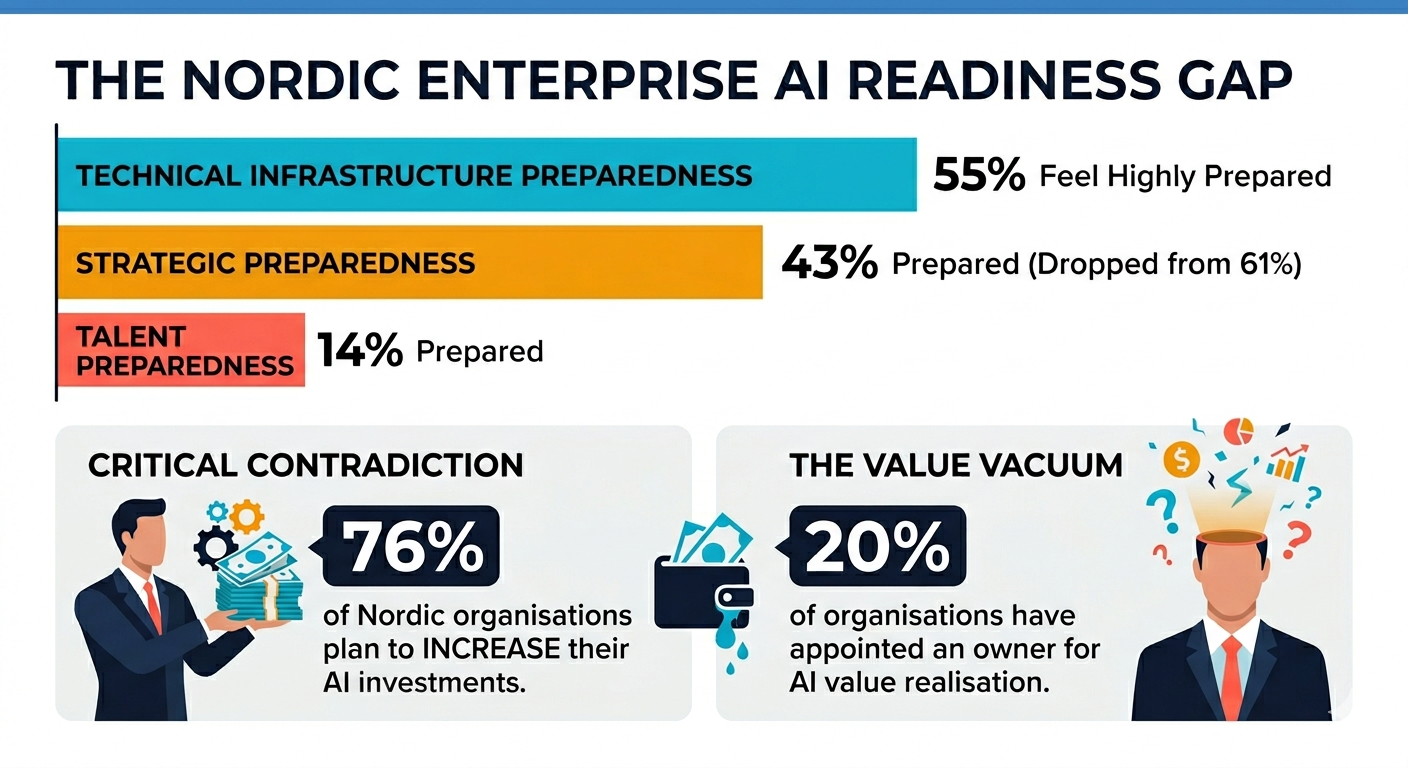

Deloitte’s Nordic findings describe a similar situation at the regional level. Nordic organisations report relatively strong technical readiness, but weaker strategic and talent preparedness. According to Deloitte, 55% of Nordic organisations feel highly prepared in technical infrastructure, while strategic preparedness has fallen from 61% to 43%, and talent preparedness has dropped to 14%. At the same time, 76% of Nordic organisations plan to increase AI investment (Deloitte 2026).

Our observations in FAIR’s AI consultancy show a similar pattern in Finland, where technical readiness similarly outpaces strategic and organisational preparedness.

The split that is already happening

The Finnish corporate landscape is splitting into two. While the share of advanced AI companies has more than quadrupled in two years, more than half of organisations still remain in the assessment and preparation phase. The earlier broad middle category has almost disappeared (Demos Helsinki 2026).

This indicates that AI adoption is becoming a divider between companies. Some companies are moving AI into products, services, and core business processes. Others remain in preparation mode. This division is visible between industries and company sizes.

AI is moving from individual tools to core business operations. Nearly half of the frontrunner companies are productising AI for customers or have integrated AI into their products. These companies also invest more and measure success more systematically than companies that focus only on internal process or customer-service development (Demos Helsinki 2026).

This is an important shift. In many public discussions, AI still appears mainly as a tool for writing, summarising, coding, or searching. In the frontrunner data, however, AI is increasingly part of what companies sell, how they differentiate themselves, and how they create value.

Efficiency is real. Transformation is rarer

FAIR’s 2026 survey gives a grounded view of what AI-active Finnish companies are actually getting from AI. The most common business benefit, reported by 73% of respondents, is streamlining internal processes and saving time (Asikainen 2026b).

Other benefits include documentation, reporting, and meeting notes (28%); new business or AI as part of a product or service (25%); information retrieval and expert work (24%); quality improvement (21%); and faster software development (21%). AI is already useful in everyday business work. But the most common benefits are still operational rather than transformational.

Recent European firm-level evidence similarly finds that AI productivity gains concentrate in firms capable of complementary investments in software, data, and workforce training (Aldasoro et al. 2026). The Finnish picture reflects this. Among AI-active Finnish companies, 85% have adopted AI within the past three years — but although AI has moved from experimentation to practical application, its use in many organisations remains at an early stage.

Deloitte’s Nordic findings align with this. In the Nordics, 79% of organisations report improved efficiency from AI, but only 18% currently achieve revenue growth from AI, even though 75% expect AI-driven revenue impact. Deloitte also notes that only 20% of organisations have appointed someone responsible for value realisation from AI initiatives (Deloitte 2026).

The picture looks similar at the individual level. Statistics Finland’s February 2026 survey found that Finnish workers using AI save an average of 5.5 hours per month — a figure that is real, measurable, and almost entirely invisible at the organisational level. No one is aggregating it, and no one is accountable for scaling it (Kangassalo 2026).

Physical AI as a distinctive opportunity

AI Finland’s report highlights particular potential in physical AI — applications embedded in or connected to real-world systems such as machines, sensors, medical devices, production lines, and industrial environments, where AI analyses physical-world data or supports decisions and automation in physical processes.

Health technology and manufacturing stand out in the initiatives and investments of frontrunner companies. Computer vision, predictive analytics, and digital twins are reported as technologies whose competitive advantage cannot be replaced by code alone (Demos Helsinki 2026).

AI is being used for automatic transcription of patient consultations, medical image analysis, diagnostic support, and analysis of large-scale medical datasets to improve clinical decision-making and medication safety. Health technology companies in the data emphasise machine learning and machine vision applications, rather than only generative AI (Demos Helsinki 2026).

These findings align with our prior AI consultancy findings in FAIR (Khan 2025a; Khan et al. 2025b), which show that healthcare organisations are particularly drawn to AI solutions due to their data-rich environments and the potential for significant impact on patient outcomes and operational efficiency.

Industrial AI is another important area. AI integrated into devices, machinery, and sensors is used for production, measurement, quality control, defect detection, predictive maintenance, and digital twins. Approximately 15% of all companies — and nearly a quarter of SMEs that participated in the AI Gala or applied for seed funding — develop or use AI integrated into the physical world (Demos Helsinki 2026).

Generative AI is important, but AI in healthcare, manufacturing, machinery, sensors, and industrial processes is also central to the national picture. Finland’s industrial history and healthtech expertise provide a foundation that purely software-driven countries cannot easily replicate. Physical AI does not compete in the same markets as the large language model ecosystem, and that is precisely why it may offer Finland a more sustainable basis for competing in the AI landscape.

Experts at Aalto University have also repeatedly highlighted that Finland’s decades of experience with targeted AI solutions could become a significant export product and offer an alternative to the resource-intensive development of large language models. (Asikainen 2026c)

Limited readiness for Agentic AI

Deloitte’s report shows that Nordic organisations have made progress with generative AI, but agentic AI and physical AI remain in their early stages. Only 5% of Nordic organisations report high expertise in agentic AI, and 49% expect agentic AI transformation to be more than three years away. Physical AI is also approached cautiously, with only 8% expecting integration within two years (Deloitte 2026).

These findings are relevant for Finland. Simply buying AI assistants or building point automations can create only an illusion of benefits if the end-to-end system of value creation is not redesigned (Demos Helsinki 2026).

It is not that every company should immediately deploy agentic AI. Rather, the next stage of AI will require more than tool adoption. It will require changes in processes, roles, governance, and business ownership. Research on robot adoption and organisational capital shows why this is structurally difficult. Productivity gains emerge only after organisational restructuring, and firms typically experience a period of deteriorating organisational capital during the transition before benefits materialise (Rodrigo 2022).

Importance of Hands-On Support

The FAIR customer analysis adds an ecosystem perspective. The report describes FAIR companies as microenterprise-dominated. Around 70% have 0–5 employees, around 76% are located in Helsinki, Espoo, or Vantaa, and the typical FAIR company is a microenterprise in software, consulting, or professional services, with revenue under €500k or not yet established.

The same analysis shows strong development among FAIR companies. Between 2020 and 2024, FAIR companies’ revenue grew by 76%, or €113 million in absolute terms, while headcount grew by 30%, from approximately 1,154 to 1,501 employees. The report states that FAIR companies grew revenue and headcount significantly faster than both the national average and the ICT-sector benchmark.

However, while FAIR builds AI and digital capability, direct financial returns are limited or harder to quantify. The most commonly reported positive impacts are AI solution development and digital knowledge and capability development, while revenue, investment, and sustainability effects are less common and often not attributed directly to FAIR.

Hands-on consulting, piloting, skills development, and financing support are important, especially for small companies with defined AI needs. But the path from support service to measurable financial impact is not automatic.

Underutilised Research Collaboration

Finland’s research infrastructure for AI is genuinely strong, encompassing the LUMI supercomputer and the ELLIS Institute for top-level AI research. Yet the bridge between this infrastructure and commercial AI development remains narrow.

Only 20% of Finnish companies engage in research or development cooperation with universities or research institutes, and 62% report no such collaboration at all. R&D cooperation is 9 percentage points more common among large companies (27%) than among SMEs (18%), which represents a meaningful disparity given that small companies dominate the Finnish AI ecosystem (Demos Helsinki 2026). Where collaboration does exist, it tends to be small in scale and project-based, with funding arrangements often ending before genuine partnerships have time to develop.

This matters because companies engaging in research collaboration productise AI solutions significantly more often than others. Research collaboration is therefore not a peripheral concern; it is one of the clearest available pathways from AI experimentation to AI business value, and it remains largely untaken. Strengthening it through longer-term partnership models, rather than short-cycle project funding, could be a potentially decisive accelerator for Finland’s AI transformation.

Authors

Dr Umair Ali Khan

Senior Researcher

Finnish AI Region

umairali.Khan@haaga-helia.fi

Martti Asikainen

Communications Lead

Finnish AI Region

martti.asikainen@haaga-helia.fi

References

Aldasoro, I., Gambacorta, L., Pal, R., Revoltella, D., Weiss, C. & Wolski, M. (2026). AI adoption, productivity and employment: Evidence from European firms. EIB Working Paper 2026/02. European Investment Bank. https://www.eib.org/files/publications/20250383-130126-economics-working-paper-2026-02-en.pdf

Asikainen, M. (2026a, April 15). The Problem Is the AI Strategy — or Rather, the Lack of One. https://www.fairedih.fi/en/2026/04/15/the-problem-is-the-ai-strategy-specifically-the-lack-of-one/

Asikainen, M. (2026b, April 30). Finnish firms embrace AI rapidly, but regulatory knowledge lags far behind, survey finds. Finnish AI Region. https://www.fairedih.fi/en/2026/04/30/finnish-firms-embrace-ai-rapidly-but-regulatory-knowledge-lags-far-behind-survey-finds/

Asikainen, M. (2026c, tammikuu 26). Finland eyes specialised AI as next major global export. Finnish AI Region. https://www.fairedih.fi/en/2026/01/26/finland-eyes-specialised-ai-as-next-major-export/

Asikainen, M., & Masala, S. (2026, May 20). AI is nearly free. That’s why we’re making our most expensive mistakes right now. Finnish AI Region. https://www.fairedih.fi/en/2026/05/20/ai-is-nearly-free-thats-why-were-making-our-most-expensive-mistakes-right-now/

Chan, C.Y.C., & Shedania, K. (2026). The aggregation paradox of AI: Why do micro-economic productivity gains from AI disappear at scale. ILO Research Brief. International Labour Organization. https://doi.org/10.54394/00034342

Deloitte. (2026). State of AI in the Nordics 2026. Deloitte. https://mkto.deloitte.com/rs/712-CNF-326/images/State-of-AI-in-the-Nordics-2026.pdf

Demos Helsinki. (2026). AI in Finnish business 2026. AI Finland; Business Finland. https://aifinland.fi/wp-content/uploads/2026/04/AI-in-Finnish-Business-2026.pdf

Kangassalo, P. (2026, May 20). Valtaosa työssä käyvistä hyödyntää tekoälyä – neljä viidestä arvioi töiden nopeutuvan. Statistics Finland. https://stat.fi/tietotrendit/artikkelit/2026/Valtaosa-tyoessae-kaeyvistae-hyoedyntaeae-tekoaelyae-neljae-viidestae-arvioi-toeiden-nopeutuvan

Khan, U. A. (2024, December 19). How to adopt AI to get real business value? Finnish AI Region. https://www.fairedih.fi/en/2024/12/18/how-to-adopt-ai-to-get-real-business-value/

Khan, U. A., & Asikainen, M. (2026, February 5). How (not) to destroy your business with AI. Finnish AI Region. https://www.fairedih.fi/en/2026/02/05/how-not-to-destroy-your-business-with-ai/

Khan, U. A. (2025a, August 25). The 2025 state of AI readiness in FAIR customer companies: The case of Finland. Finnish AI Region. https://www.fairedih.fi/en/2025/08/25/the-2025-state-of-ai-readiness-in-fair-customer-companies-the-case-of-finland/

Khan, U. A., Kauttonen, J., & Kudryavtsev, D. (2025b). AI adoption in Finnish SMEs: Key findings from AI consultancy at a European Digital Innovation Hub. 2025 IEEE 23rd World Symposium on Applied Machine Intelligence and Informatics (SAMI), 465–470. https://doi.org/10.1109/SAMI63904.2025.10883271

Rodrigo, R. (2022). Robot Adoption, Organizational Capital, and the Productivity Paradox. Working Papers gueconwpa~22-22-03. Georgetown University. https://ideas.repec.org/p/geo/guwopa/gueconwpa~22-22-03.html